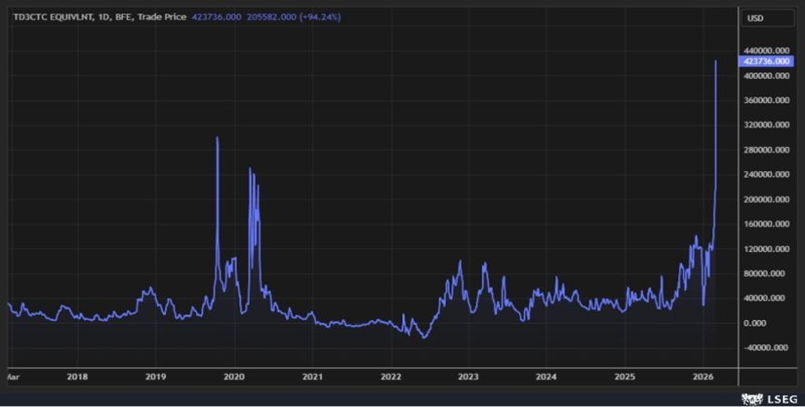

Against the backdrop of a sudden escalation in the Middle East situation and disrupted shipping through the Strait of Hormuz, VLCC spot market freight rates have surged to an all-time high. According to Tankers International, a leading tanker pool operator, the Pantanassa—a 2011-built Very Large Crude Carrier (VLCC) of 317,000 DWT owned by established Greek shipowner Minerva Marine—has been fixed at a record spot rate exceeding $400,000 per day by South Korean refining giant GS Caltex.

Shortly afterwards, SSY confirmed this blockbuster fixture. Its data shows the Pantanassa has a cargo capacity of 270,000 metric tons, is expected to commence loading on March 28, at a fixture rate of WS450.

This figure not only breaks the all-time high in the global VLCC spot market but also signals that global crude ocean freight costs have entered an era of extreme volatility under intense geopolitical pressure.

Transaction Details

Market sources indicate that the 317,000 DWT VLCC Pantanassa (built 2011), owned by Greek shipowner Minerva Marine, was recently chartered by South Korean refiner GS Caltex for a voyage loading crude at Yanbu, a Red Sea port in Saudi Arabia.

According to Tankers International, based on a voyage duration of approximately 60 days, the equivalent earnings stand at around $436,000 per day, with a total voyage freight of about $26.2 million. This level is far above the normal range of the VLCC market in recent years, and also breaks the previous record of around $307,000 per day set in 2019 amid sanctions on COSCO-related entities, making it the highest daily earnings level ever recorded in the VLCC spot market.

Direct Cause of Rate Surge: 8% Drop in Effective VLCC Capacity

From a broader tanker freight perspective, the conflict involving Iran and the blockade of the Strait of Hormuz have directly caused a sharp contraction in available tanker capacity in the Middle East.

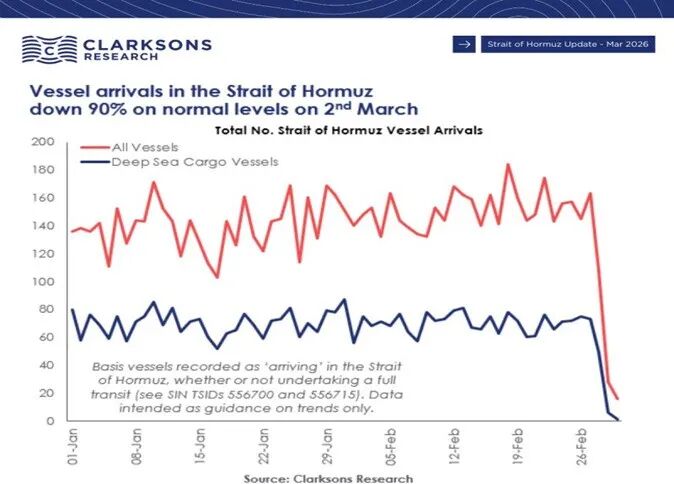

Data from Clarksons shows that within days of the conflict, traffic through the Strait of Hormuz plummeted by 94%. At least 200 tankers engaged in legitimate international trade—including 60 VLCCs, roughly 8% of the global compliant VLCC fleet—were forced to anchor at terminals inside the Persian Gulf or loiter outside the Gulf of Oman.

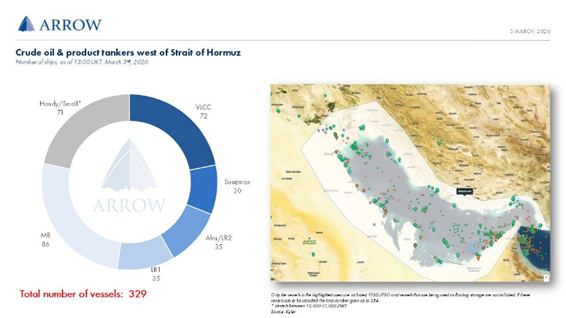

Shipbroker Arrow reached the same conclusion, noting that 329 crude and product tankers are currently stranded in the Middle East Gulf, waiting as they cannot safely transit the Strait of Hormuz. Among them, 72 are VLCCs, accounting for approximately 8% of the global VLCC fleet—equivalent to a large block of effective capacity being directly “removed” from the trading fleet.

This massive effective supply that once circulated globally vanished instantly, giving birth to this epic freight rate rally.

Tight Demand & Widespread Panic: Shippers Bear Over 16% Extra Cost

Facing a steep drop in supply, demand has become inelastic due to extreme panic. For instance, Asian refiners such as GS Caltex would face shutdowns across their entire petrochemical supply chain if crude supplies were cut off—economic losses and restart costs far outweigh the high freight expenses.

As a result, charterers are desperately seeking the few vessels willing to enter the war zone to load cargo.

Based on the fixture rate of $436,000 per day, a standard VLCC can carry approximately 2 million barrels of crude. Spreading the total $26.2 million freight across the cargo means the pure ocean cost per barrel has soared to $13.10.

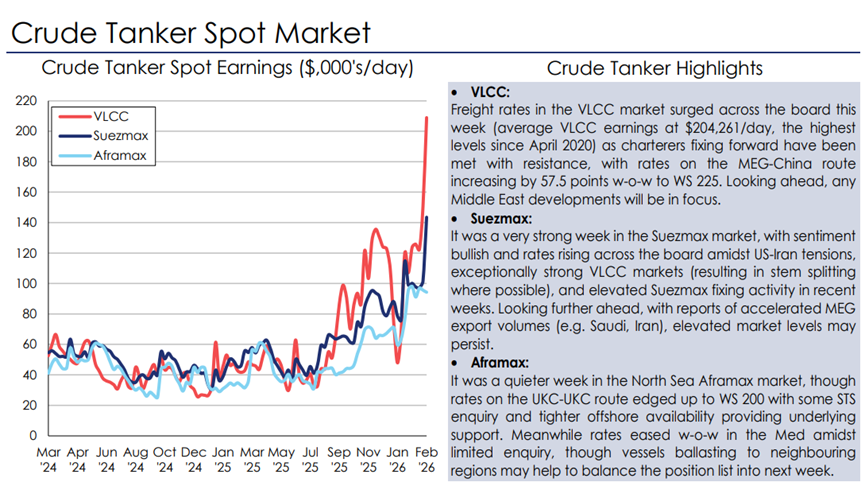

By comparison, from late 2025 to early 2026—before the full escalation of the Middle East conflict—the benchmark daily time charter rate for VLCCs on the Middle East–Asia route fluctuated only between $40,000 and $60,000. Under normal market conditions, per-barrel crude ocean freight typically ranges narrowly from $1.50 to $2.50. Even during peak demand or occasional tightness (around $170,000 per day), per-barrel freight was only about $8.50.

This means GS Caltex is forced to pay 5–8 times the normal average rate. With Brent crude at around $80 per barrel, this freight adds a supply chain premium of over 16% to already thin refining margins.

The extreme supply–demand imbalance has created a distorted market: soaring theoretical rates but very few actual fixtures. The $436,000 quote—or $431,800 as assessed by the Baltic Exchange—does not reflect a liquid market trading at these levels, but rather a market breakdown.

In reality, it is a theoretical valuation driven by extreme panic, military blockades, and insurance disruptions. As long as the conflict continues, physical trade cannot recover, and the global energy supply chain will remain shaken under these inflated theoretical levels.

Full-Scale Contagion Effect

Clarksons sharply noted in its report:

“Although the conflict mainly affects Middle East routes, freight assessments on other routes are also rising.”

This reveals the classic substitution effect and capacity crowding-out effect in shipping.

As Middle East crude faces physical blockades and insurance disruptions, panicked Asian buyers (China, India, South Korea) have quickly turned to alternative supplies in the Atlantic Basin—such as WTI crude from the US Gulf and pre-salt crude from Brazil. This panic-driven inter-regional buying has exploded demand for Atlantic capacity. Consequently, the DHT Puma achieved round-voyage earnings of $285,000 per day on the Brazil–Asia route.

Meanwhile, VLCCs (2-million-barrel class) are monopolized by Sinokor and extremely scarce, forcing charterers to downsize to smaller Suezmax (≈1 million barrels) and Aframax (≈600,000 barrels) tankers. This spillover effect has ignited the medium-sized tanker market. In early March, Suezmax spot freight from the Middle East to China rose to WS525, with daily earnings surpassing $300,000. Aframax regional short-haul freight has also doubled.

One-off Spike or Structural Inflection Point?

From a historical perspective, the $436,000 milestone is fundamentally different from previous tanker rate spikes.

A horizontal comparison with major recent market dislocations:

· The 2019 record of $307,000 per day stemmed from OFAC sanctions on COSCO subsidiaries involved in Iranian trade, causing global charterers to blacklist those vessels over compliance fears. This was merely a one-off spike from a 3–5% reduction in compliant capacity; the market corrected within weeks, with rates crashing to $96,000.

· The 2020 high was driven by pandemic-induced demand collapse, with crude in storage and tankers repurposed as “floating storage,” tightening shipping supply.

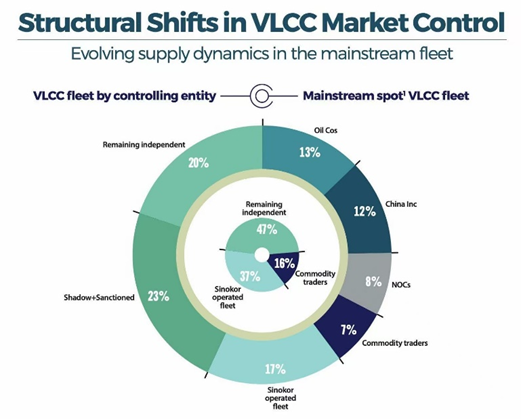

In contrast, the 2026 $436,000 level is not just a short-term black swan but an inflection point—likely far more persistent than past quick corrections. On one hand, it reflects an absolute physical shortage caused by prolonged conflict, hard channel blockades, and the breakdown of modern shipping finance and insurance. On the other, the VLCC market has seen an unprecedented oligopolistic concentration led by South Korea’s Sinokor. The geopolitical conflict has ignited this tightly controlled market, creating an unprecedented and sticky price inflection.

Deep reports from maritime data providers including Signal Ocean and Veson reveal that following an investment of over $2.5 billion, Sinokor’s share of the compliant VLCC spot market has surged to an alarming 24%, with its controlled spot fleet approaching 150 vessels.

In a historically fragmented market where the top 10 owners held just 48% of capacity, this concentration has broken the balance of modern shipping history. At the outbreak of the conflict, the dominant Sinokor used its pricing power to quote charterers as high as WS700 (≈$20 per barrel). Sinokor is not only the biggest beneficiary of the geopolitical crisis but also the key driver inflating the freight bubble through capacity monopoly.